Chargeback Management

Watch this video to understand how chargebacks are handled in Chargebee.

What is a chargeback?

A chargeback is a dispute raised for a payment made by the customer. Although it appears similar to a refund, there is one major difference between the two. In the case of a refund, the merchant reverses the funds to the customer. In a chargeback, the customer disputes the transaction with the bank directly. The money is deducted from the merchant's business account and returned to the customer. The merchant or business owner is notified only after the amount is deducted.

Types of chargeback

There are three types of chargebacks:

Merchant error

When the customer's card is mistakenly charged for a subscription or product that was already canceled.

Here are a few examples of merchant errors:

- The cancel option is not easily discoverable on the website, or the cancellation process is tedious.

- The buyer is not happy with the product or service.

- To avoid a cumbersome return process.

- Recurring payments go through even after canceling the subscription.

- The return time for the product has been exceeded.

Criminal fraud

Unauthorized transactions on the card made by fraudsters or hackers.

Here are a few examples of criminal fraud:

- The customer does not recognize the transaction.

- Unauthorized charge on the card.

Friendly fraud

Friendly fraud is the process of filing a chargeback directly without contacting the merchant for a refund. Cardholders often dispute a legitimate charge on their credit card to receive a refund from the bank.

Here are a few examples of friendly fraud:

- Does not want to pay for the product.

- To avoid a restocking or handling fee.

Chargeback process

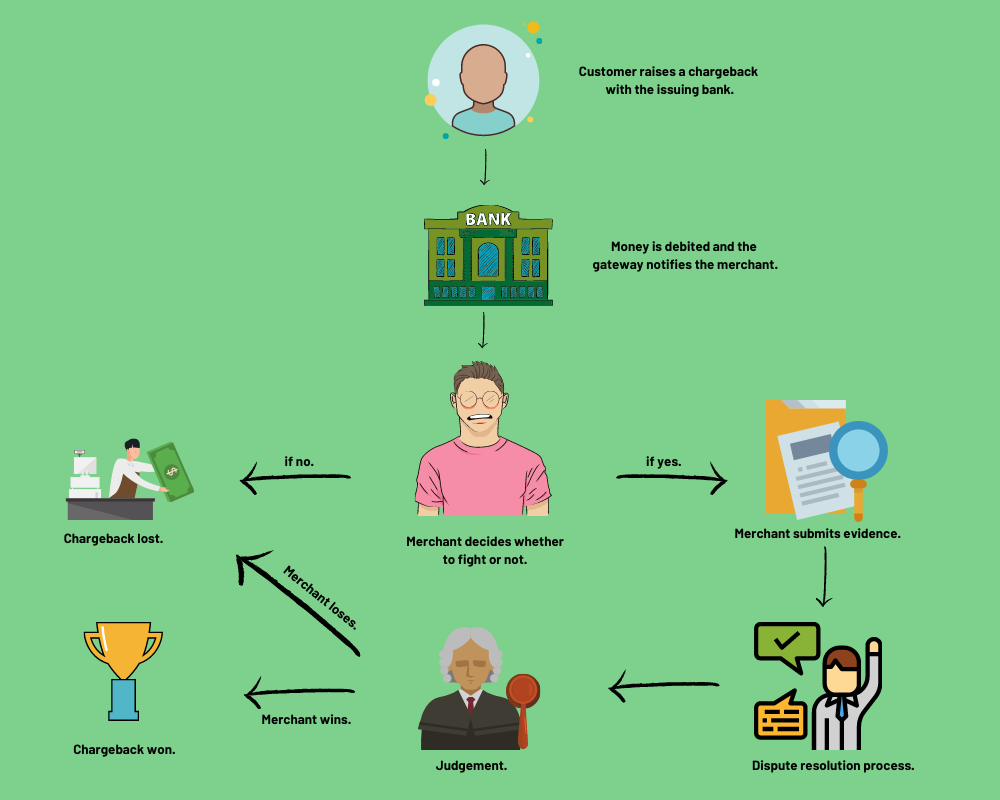

When a customer files a chargeback dispute with the issuing bank, the issuing bank contacts the acquiring bank and informs them of the chargeback. The customer can raise a chargeback anytime between 45 and 180 days (up to 13 months for SEPA), depending on the payment method and the bank's terms. The acquiring bank debits the amount from the merchant's account.

Once the funds are debited from the merchant's account, an alert is sent to the merchant. A reason code is mentioned in the alert, which helps the merchant identify the cause of the chargeback. The merchant has two options: dispute or accept the chargeback. If the merchant decides that the claim is legitimate or chooses to accept the chargeback, the chargeback is considered lost.

If the merchant has provided the required service or product and wishes to dispute the chargeback, they must provide evidence to validate or disprove the dispute. The merchant is generally given 7 to 10 days to submit the evidence. The dispute then goes through a resolution process, which can take approximately 30 to 90 days. If the evidence is valid, the merchant wins the chargeback; if not, they lose the chargeback.

Payment gateways supported for Chargeback Management

Chargebee supports chargeback management for card and SEPA payments only. The following payment gateways are qualified to handle the chargeback management process:

- Stripe

- Adyen

- GoCardless

- Mollie

- EBANX

- Pay.com

- Braintree

- Checkout.com

Chargeback workflow in Chargebee

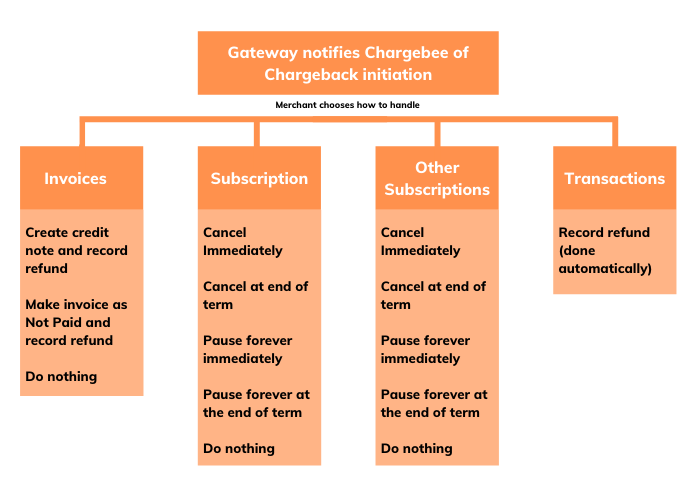

Chargebee supports chargeback management at two stages: Chargeback initiation and Chargeback lost.

Once the money is debited from the merchant's account, the payment gateway notifies Chargebee via a webhook. At this stage, the merchant can choose to automatically record the refund (that was debited because of the chargeback) and decide how to handle invoices and subscriptions of the customer until the dispute resolution is obtained.

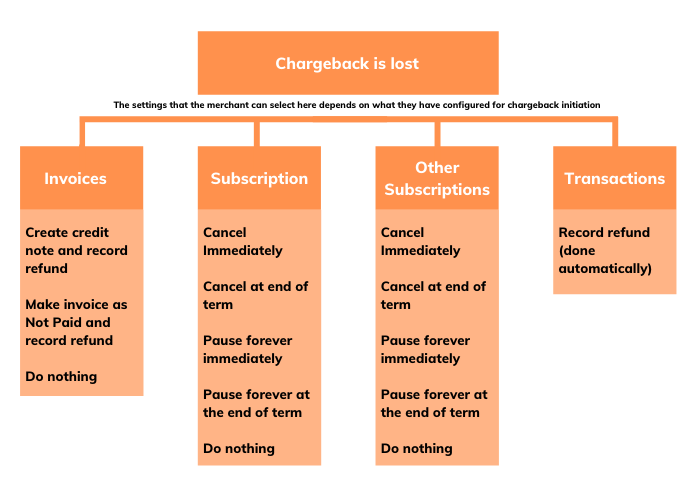

The merchant can configure settings in Chargebee to handle chargebacks that are lost. This is explained in detail in the next section.

If the chargeback is won, the merchant must intervene and manually change the impacts across the subscription and invoice module.

Refer to this document for detailed information on configuring chargeback management.

Limitations

Chargeback management is not possible for the following cases, as they require manual intervention from the merchant:

- When an invoice has a credit note associated with it.

- Partial disputes associated with consolidated invoicing.

- Partial disputes related to a single payment (transaction) made to collect the amount for multiple invoices (using Pay Now option).

- Disputes associated with gift subscriptions.

- When the chargeback is won.

- If the currency of the transaction in Chargebee does not match the currency of the dispute that is raised.

- If the dispute amount is greater than the transaction amount.

Frequently asked questions

-

Is it mandatory to enable webhooks in Stripe for Chargeback events to work in Chargebee?

Yes. To ensure that Chargeback events are accurately tracked and reflected in Chargebee, specific webhooks must be enabled in your Stripe account:

-

For Chargeback Initiated events,

enable the charge.dispute.funds_withdrawnwebhook. -

For Chargeback Closed events,

enable the charge.dispute.closedwebhook.Enabling these webhooks ensures that Chargebee can receive and process chargeback updates from Stripe in real time.

-

Why isn't a Chargeback dispute created in Chargebee for some Adyen or Mollie payments?

If you see that a chargeback is raised at the gateway (such as Adyen or Mollie) but no dispute appears in Chargebee, it's likely because the event is not a true chargeback. Some gateway-reported reason codes actually indicate late payment failures, not chargebacks. Chargebee only raises disputes for recognized chargeback codes. All other codes are treated as non-disputable events to avoid unnecessary dispute handling on your end.

Chargeback Code Reference

Gateway Chargeback Codes Mollie SEPA MD06 Adeyn SEPA MD06, MS02, MD01 Adyen BACS 1, 4, 7, 8, 9, D Adyen ACH R51, R31, R29, R11, R10, R08, R07, R05

Articles & FAQs

Was this article helpful?