47Credit card processingFacts, Statistics, And Trendsevery online merchant should know

Chapter 1Outlook

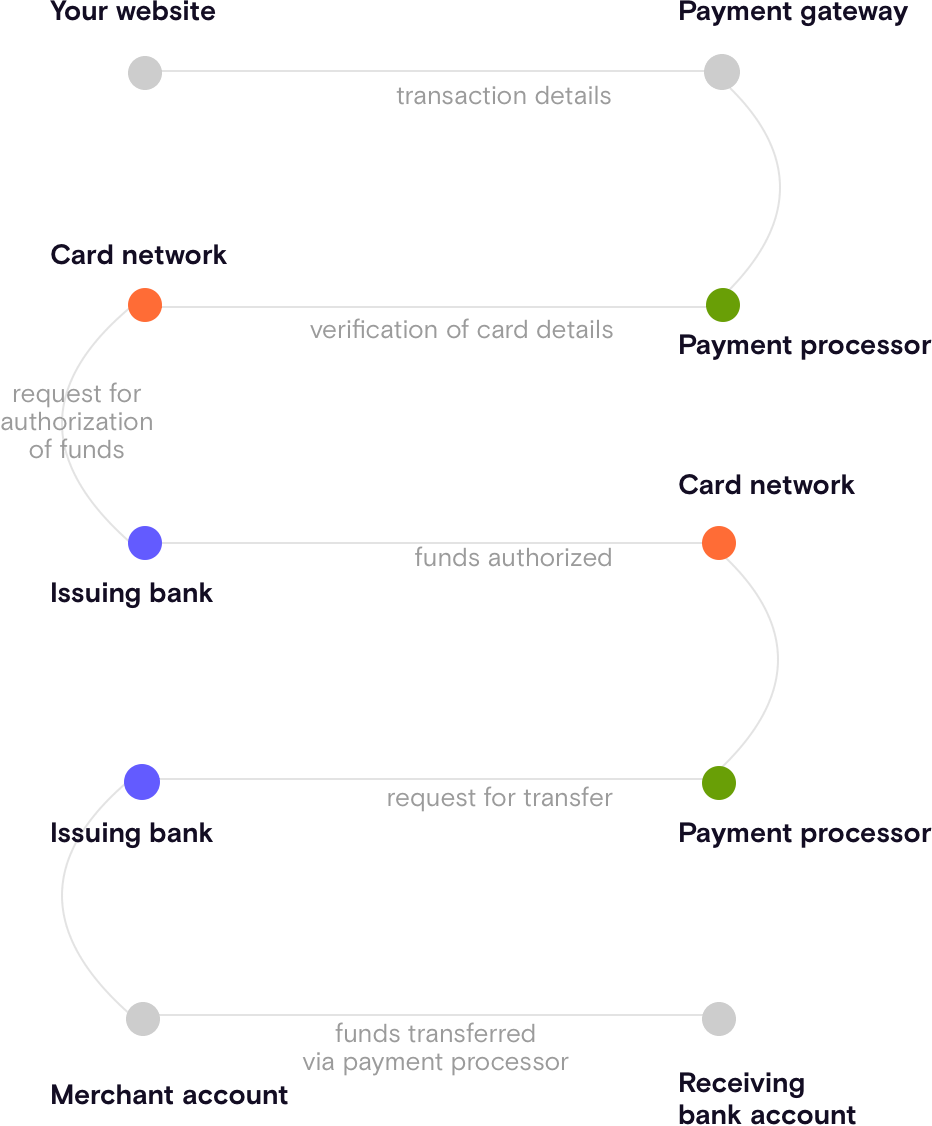

From what online credit card processing involves to who the players with skin in the game are, what the credit card market looks like, and what the state of online payments is today, here's an overview of what you need to know if you are thinking of taking your business online or setting one up from scratch.

1A. The credit card market today

The players and the playing field

The Credit Card Market

160millioncredit cardholdersin the US.CFPB Consumer Credit Card Market StudyWorldwide credit card circulation

14.4 billion credit cards

in the world (as of 2017) The Nilson Report

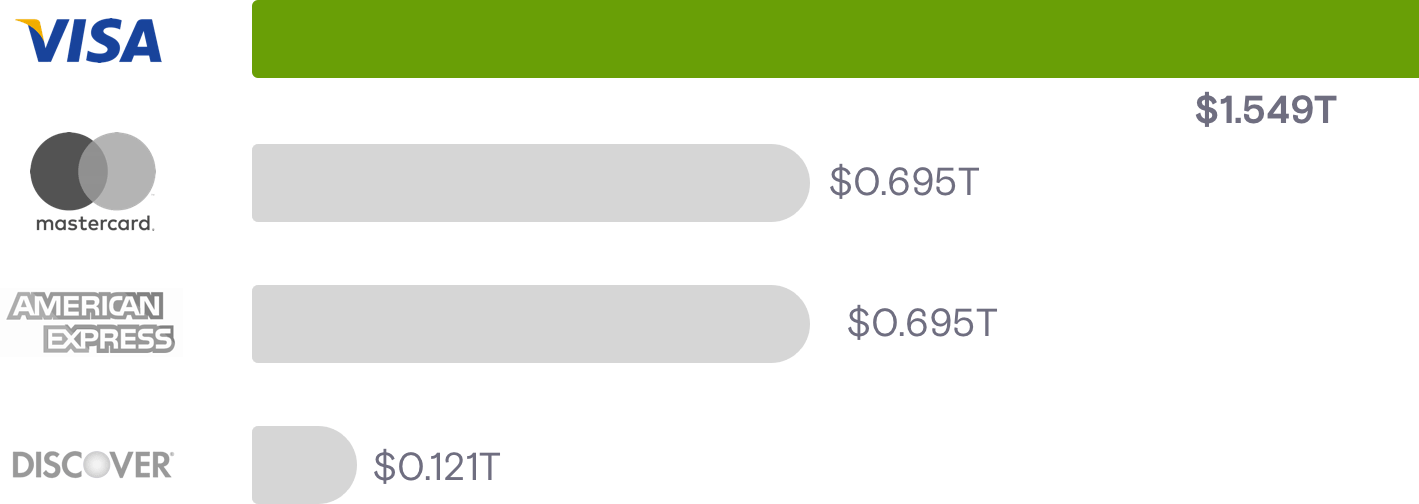

The Nilson ReportTop card networks in the U.S.

The Nilson Report

The Nilson ReportWho issues credit cards in the US?

Organizations responsible for the funds do.

A bank, in most cases. Although, some financial institutions like American Express, for example, operates as issuer and network.

Forbes

ForbesNumber of active credit cards/person

Card-holding consumers with average credit scores (620+) have atleast

4 active credit cards.CFPB Consumer Credit Card Market StudyDid you know?

500,000applications for credit cards/day

(US Consumers)

CFPB Consumer Credit Card Market StudyConsumers are using their credit cards more than they did

Average Credit Balance

$4800The highest it's been since

2005.CFPB Consumer Credit Card Market StudyOnline payments are growing

(2013 to 2017)Online payments in the US have grown 4 times as much as retail payments

It has grown by ~64% in the last four years.

US Census Bureau News 2017

1B. How are online sales doing?

Online sales are strong

(U.S. Consumers - last year)9/10say they have made at least one online purchase in the past 12 months.

7/10made three or more online purchases in the last year.

5/10say they have increased the frequency of their online purchases in the last year.

American Express Digital Payments SurveyOnline sales are strong

~19.Number of

online transactions per person per year.KPMG Global Online Consumer ReportWhat are merchants saying?

Compared to previous years, 71% merchants say

Annual Sales(online and mobile)

are increasingAmerican Express Digital Payments surveyA look at spending habits

U.S. Consumers spend

12–18% MOREwhen using credit cards instead of cash for purchases

Dun and Bradstreet survey

Chapter 2Safety

Arguably the biggest question on a merchant's mind. Is online credit card processing safe? The truth is there are nuances to consider before you decide. While the data reveals that online attacks and friendly fraud are both getting worse by the day, the tools and infrastructure to combat them are getting sharper. The issue is how much the tools cost and how difficult it is to keep up with regulation that is constantly being updated. What does the state of fraud mean for small businesses? Where does it leave your customer relationships?

2A. The fraud panorama

Fraud trends in the U.S.

America is responsible for about a quarter of the global card transaction volume. But, it accounts for nearly half of worldwide credit card fraud.

If you are selling in the U.S. Think about fraud

QuartzA look at the numbers

The costs of credit card fraud have increased by

26%(U.S. 2013 to 2017)

Federal Trade commission's' Consumer Sentinel Network Data Book, 2017Online vs in-person fraud

The scales tipped in 2016 for the first time in credit card history

Online fraud accounted for 58% in 2016

Federal Reserve Payments Study — 2017

Federal Reserve Payments Study — 2017Does the size of your business matter to a fraudster?

The size of your business doesn't matter

to the online fraudster.Attacks targeting businesses with less than 250 employees are expected to grow in 2018.

Internet Security Threat Report 2016Not all online fraud is created equal

Routinely reported friendly fraud rates

60%–90%(Online merchants – 2016)

Friendly fraud is the case of a customer receiving a service only to provide invalid card details or false information.

Solving the CNP False Decline Puzzle — Ethoca Research ReportChargebacks contribute to fraud too

Friendly fraud = Chargebacks

Online Merchants Chargeback losses

$7B–2016This number is expected to be 4x larger in 2020.

Payment Fraud Outlook 2020

2B. Does safety impact customer relationships?

Consumers don't believe their information is safe

Only 1/10 Americans are 'very confident' that websites are capable of keeping their credit card information secure.

Pew Research Center SurveyDid you know?

7/10consumers make payment decisions based on which payment method is most secure.

Cardtronics Health of Cash, 2017Security concerns can impact sales

37%say they have abandoned an online purchase because they did not feel their payment would be secure.(Consumers who have made three or more online purchases in the last year)

American Express Digital Payments Survey

2C. Fighting fraud

The most effective tools to fight fraud

AVS Filters

(Address Verification Service)

CVV Filters

(Card Verification Numbers)

Rated by merchants in the U.S.

Fraud Benchmark Study, CyberSourceEffective fraud tools are underused

only53%of merchants require customers to enter the CVV

only39%decline transactions when a verified billing address has not been provided.

American Express Digital Payments SurveyCompliance regulations are frequently updated

62% of financial service firms are expecting regulators to revise regulatory information in 2018.

(22% are expecting new regulation)

Cost Of Compliance Study, Thomson Reuters, 2017Keeping up with regulations is difficult

Only 31% of

businesses outsource their compliance to a third party.Cost Of Compliance Study, Thomson Reuters, 2017Does it make sense to outsource compliance?

Of the businesses who outsourced compliance in 2017, the 38% said it was because of the rising cost of compliance.

(This number was 24% in 2016)

Accenture Cost of Cybercrime study 2017Does it make sense to invest in security intelligence?

Investing in security intelligence systems saved online businesses $2.8 million in 2017

Accenture Cost of Cybercrime study 2017

Chapter 3State

Credit cards have been a go-to payment method since long before the internet was around. This is slowly changing (finally). Mobile payment adoption is on the rise, e-wallets are predicted to take over the online payment market in the next decade or so, and direct debit payments are a preferred payment method in Europe. Does this mean it is not worth accepting credit cards in 2018? The answer is more intricate than you might think.

3A. Multiple payment methods matter

Cash on the decline

2/3of merchants say that they are very likely to go completely cashless in the near future.

American Express Digital Payments SurveyCheck payments are on the decline

By 2018,

check payment volume

will reduce by46%Nilson Report, Growth in Purchase Transactions 2009 – 2019Did you know?

9/10people like having the ability to use a variety of payment methods when making a purchase.

Cardtronics Health of Cash reportPayment methods are important to customers

(Of the consumers who make an online purchase at least once a week)

73% reveal that the type of payment a business accepts impacts whether they will buy from that business.

JP Morgan Chase Report — The Intersection of Payment and Commerce in a Digital World

3B. Alternative Payment Methods

How are alternative payment methods doing?

E-wallets will grow the most as a payment method in the next five years

(Compared with bank transfers, cash on delivery, charge cards, debit cards, PostPay, PrePay, and others)

WorldPay, Global Payments Report PerviewE-wallets are the future, but they're not there as yet

(As of 2018)

Only 16% of

consumers have ever used e-wallets.JP Morgan Chase Report — The Intersection of Payment and Commerce in a Digital WorldPayPal is the e-wallet of choice

is the most recognized and used online checkout service77% of the cardholders in the USare familiar with the service.

62% of the cardholders in the US are familiar with and are currently using the service.

69% of consumers believe Paypal's technology is better at protecting their financial information.

Globe News Wire Survey 2016Credit cards are more popular than ever

(2015–2017)

Credit card payments registered the highest growth rate

10.2%among the core payment types.

Federal Reserve Payments Study 2017Can cards compete with alternative payment methods?

Credit Cards are expected to be the e-wallets' only serious competition over the next five years.

Federal Reserve Payments Study 2017Merchants predict credit cards will never be out of fashion

7/10merchants believe they will still be accepting credit card payments in five years

JP Morgan Chase Report — The Intersection of Payment and Commerce in a Digital World

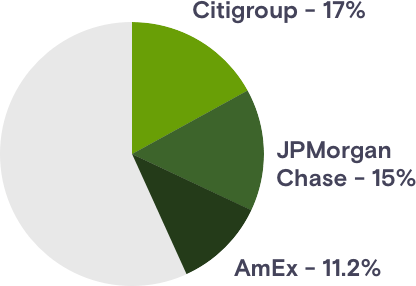

3C. Location influences preferred payment methods

UnionPay owns the growing Chinese market

While Visa, Mastercard, and American Express own the US market share, UnionPay owns the global credit card market, growing 51% from 2012 to 2017.

(UnionPay went from 3,534 million cards in circulation to 5,341 cards).

The Nilson Report — Payment Cards WorldwideDirect Debit is Europe's preferred payment method

90%of consumers with bank accounts in the UK have at least one direct debit mandate.

BACS Direct Debit Consultation Outcomes 2017

Chapter 4Costs

Last (but certainly not least), there is the question of how much it's actually going to cost you to accept payments online. Apart from the obvious costs that you will owe your gateway or merchant service provider (a cut of which will go to all the players we met in Chapter 1), there are the not-so-obvious costs that you need to plan for: from accounting to a checkout experience and ever-dreadful chargebacks.

4A. The usual suspects

A breakdown of credit card processing fees

1. Non-negotiable feesAn assessment fee is owed to the card network facilitating the transaction (Visa or MasterCard, for example). An interchange fee is owed to the bank that issued the credit card being used for the transaction.

Together, these non-negotiable fees work out to between 2% and 4% per transaction.

2. Negotiable feesAnd finally, you pay your gateway or processor a markup fee.

It's in negotiating the markup fee that you can minimize how much it costs to process credit cards.

Here's a detailed guide to processing fees and how to get the best price for your payment processor →

The cost of credit card processing fees

(Credit card processing fees paid by U.S. merchants in 2017)

$7 billionThe Nilson Report

4B. Additional overheads

Additional cost: Building a checkout experience

6/10merchants who saw an increase in online sales in 2017 said that an improved checkout experience played a significant role.

American Express Digital Payments SurveyAdditional cost: Bookkeeping

Annual costs can be anywhere from

$1,000–$20,00040% of online small business owners say bookkeeping and taxes are the worst part of running a business. 47% said that the financial cost was the biggest burden bookkeeping posed to their business.

NSBA Small Businesses Taxation SurveyAdditional cost: Fraud

8%of online revenue is at risk of fraud

Customers aren't liable if a fraudulent or erroneous charge hits their credit card account. While this is a huge part of the reason consumers find credit cards safe to use and prefer them, it can be a cost on your business if it isn't planned for.

Global Fraud Attack Index 2016

4C. Chargebacks: Another cost to think about

What are chargebacks?

A chargeback is a disputed transaction.

When a customer initiates a chargeback, she is disputing that the charge was made and is asking for her money back.

Minimum cost per chargeback

A chargeback can cost anywhere between

$5–$30(depending on your gateway; if a dispute escalates to arbitration, it can incur fees upwards of $500).

Chargeback Fees: Processor Library for Merchants (chargeback.com)Friendly fraud = Chargebacks

9/10cases of chargebacks are probable case of fraud

Federal Reserve Bank of Kansas City, Research Working Papers 2016Your chargeback rate will tell you if you're being scammed

If your chargeback rate is

Above 1%

then you might be a victim of chargeback fraudIf you divide your total chargebacks by the total number of transactions within a monthly period, you have your chargeback rate.

The average chargeback rate is around 0.5–0.8%, with an industry-standard maximum of 1%.

CyberSource Fraud Benchmark StudyThe crucial difference between chargebacks and returns

8/10customers admit to filing a chargeback out of convenience

(6 out of 10 customers admit that they're unaware of

a store's return policy at the time of purchase.)Consumer Insights Survey (chargeback.com)Chargebacks lead to losses

It's impossible to

put an exact number

to chargeback losses.Chargebacks do incur losses. A partial picture of what these losses are is possible, and it's enough to conclude that chargebacks can significantly affect a business's bottom line.

Federal Reserve Bank of Kansas City, Research Working Papers 2016