Credits touch every layer of your commercial operation: from how deals are quoted to how revenue is recognized to what customers see in their dashboards. The infrastructure behind them has to be designed end-to-end, not bolted together from tools that weren't built to talk to each other.

When any piece breaks, customers notice immediately. It's their money. Trust in a virtual currency is the product.

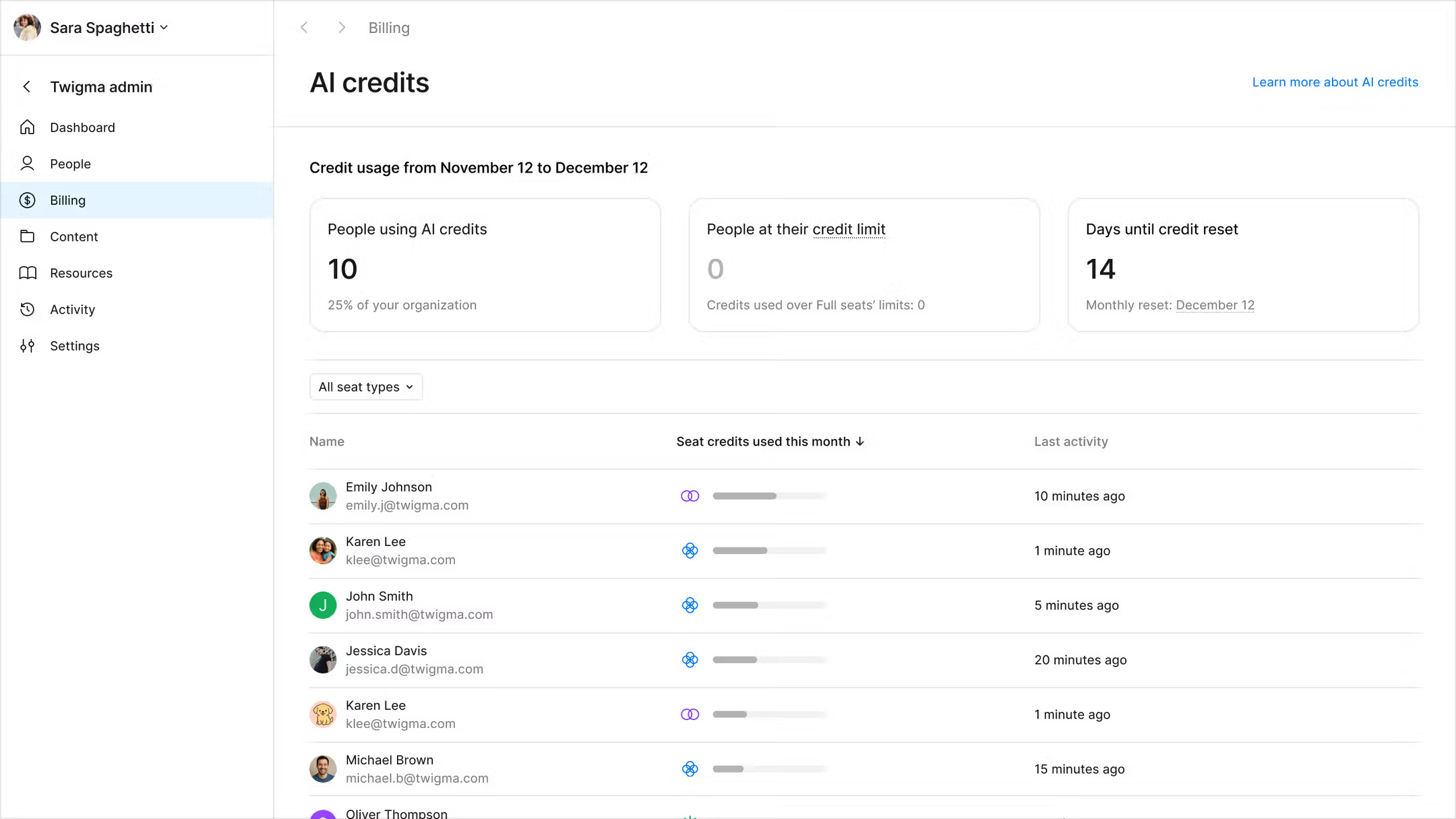

Metering: Traditional billing platforms process thousands of recurring billing events per day. Credit systems require infrastructure that handles millions continuously, so that every API call, every generation, and every agent action gets ingested, de-duplicated, and applied to the right credit block without dropping a single event or introducing lag. Most teams discover this mismatch after launch.

The credit ledger: A basic ledger sounds simple: add credits when purchased, subtract when consumed. In practice, it needs to handle multiple credit blocks, FIFO expiry logic, cost basis tracking, mid-period top-ups, and overage balances. Your ledger is your source of truth. If it can't answer exactly how many credits a customer has at any moment, your invoices, portal, and renewal conversations rest on uncertain ground.

Revenue recognition: When a customer buys credits, your business receives cash, but you haven't yet earned the revenue. Those credits sit as a liability until consumed, and under ASC 606, you need to track this with precision. Rollovers extend that liability window: allow credits to roll over once on annual contracts, and your deferred revenue window stretches to 24 months. Free and paid credits are recognized differently, with promotional credits potentially carrying a contra-revenue treatment. Get the recognition policy agreed with your finance team and auditors before you go live, not after.

The full revenue lifecycle: A credit ledger and a pricing tool are necessary but not sufficient. Credits need to flow correctly from CPQ through billing through revenue recognition. Point solutions leave you stitching these pieces together manually, and every pricing change breaks the stitching somewhere.

Most teams try to solve this by stitching together a billing platform, a separate CPQ tool, and a custom-built ledger. This approach works until it doesn't. Usually, at the moment a customer questions an invoice, your finance team needs to close the quarter clean, or you're rolling out a new pricing tier, and you realize the change lives in three different systems.

We built Chargebee for exactly this. Credit grants, real-time metering, ledger management, revenue recognition, and the customer-facing consumption dashboard are one connected system, not four tools talking to each other. When your pricing changes, it propagates. When a customer asks how many credits they have, the answer is instant. When your auditors ask about deferred revenue, the ledger answers.

That's what a credit system looks like when it's built to scale.